A Value Trap, an Ancient Stock Pitch, a Glimpse Into The Past

Anyone else out there not having very much fun these last couple of months? It feels like the bid for anything small/off-the-run has totally vanished since July. Micro-caps are down 7% year-to-date and are 35% off their June 2021 highs. It’s grim. But what do we do when the market is doing us no favors? We redouble our efforts! There is no shortage of value out there. No shortage of value, but also no shortage of value traps. One of them caught me.

Not A Bingo

For years I have held shares in Four Corners, Inc., a Texas-based supplier to charitable bingo events. Four Corners is a nice little business. From 2018 to 2022, revenues grew at a high single digit pace and earnings soared thanks to good operating leverage. The business was very capital light and lacked meaningful reinvestment opportunities, so it simply paid out nearly all its earnings in dividends, most recently paying $0.20/year. Shares hovered between $2.00 and $2.20 or so for most of the past year, offering shareholders a nice cash yield and an underlying valuation of 6x earnings for a business with zero debt and decent prospects. Having bought in around $1.50, I was pretty pleased with the company’s performance and also with myself for owning it.

Imagine my dismay last month when I saw the fateful news: Four Corners had agreed to a transaction in which it would sell virtually all its assets to another Texas bingo supplier for the equivalent of $1.9847 per share. The headline price was bad enough, giving away the company at a discount to its open market value, but the structure was the real killer. By doing an asset sale, Four Corners would be liable for taxes at the corporate level and with a cost basis substantially below that of most shareholders. End of the day, shareholders would be lucky to receive value equal to 80% of the undisturbed Four Corners share price.

I briefly considered trying to mount some resistance to the proposed sale, but the deal was done. Insiders had locked up >80% of the vote before the announcement. But why, oh why, would anyone agree to this abysmal deal? I had some suspicions, and some of them were confirmed in the proxy statement the company sent out. Sure enough, two members of the Four Corners executive team had secured continuing employment with the acquirer. No skin off their back.

So what’s the lesson here? As always, management matters, especially for tiny companies, ESPECIALLY when that tiny company is controlled by a small number of shareholders. The motivations and incentives of those shareholders may not align with those of outside investors, and when they prove detrimental, those outside shareholders may have precious little recourse. I had thought that Four Corners’ reasonable capital allocation policy and lack of the objectionable related-party transactions that plague micro-cap companies was evidence of good faith and stewardship. It was not.

My saving grace in this situation was position sizing: tiny. Despite how much I liked the business, I was reluctant to go big on the very illiquid shares of a niche business in a limited geography with relatively few customers. As an outside investor in public companies, you will never have a complete picture of what is truly going on, for better or for worse. In my time, I have had the opportunity to observe the inner workings of a couple of small public companies, including sitting in on board meetings. Comparing what I had seen, heard, and learned with what investors were saying on social media and in message board posts made me wonder: were we discussing the same company? I think this perspective is helpful in avoiding hubris. I do not and can not know everything about a company as an outsider, so tread carefully.

In this case, conflicted management turned what should have been a great investment outcome into a merely satisfactory one. I am perfectly capable of leaving money on the table through my own bad decisions. I don’t need company management to compound my errors, which is why this one hurts worse.

From The Vault

I was looking through some ancient files and I found a presentation and stock pitch I did in August, 2016. Feels like an eternity ago! I was practically a baby! The stock in question was Wilh. Wilhelmsen Holding ASA, a venerable Norwegian holding company active in the specialty shipping and offshore services industries. Here’s a link to the pitch.

Wilh. Wilhelmsen Holding ASA Quick Pitch - Alluvial Capital Management, LLC August 2016

At the time, the company was trading at NOK 160, a gigantic discount to net asset value. Reading my old stock pitch (which wasn’t bad, though I’ve made a lot of progress since!) lead me to check on how the idea actually performed. Pretty well, it turns out. Since August 2016, Wilh. Wilhelmsen HoldingsASA stock has produced a total return of 135%, or about 13% annualized. This exceeds the S&P 500 Index and beats the pants off of any European benchmark. But here’s the interesting part. My pitch, as with most involving a deeply-discounted conglomerate, was based on the company performing some type of value-unlocking transaction, like a spin-off, tender offer, or divestiture, that would cause the market to “wake up” and narrow or close the discount to asset value. Well, it’s been 7 years. The company took a few steps in that direction, merging its main shipping asset with a competitor and doing some repurchases and tender offers for its own shares and those of a subsidiary. But on the whole, the company looks much like it did in 2016. Maybe it was the distraction of an inter-family power struggle, or perhaps the Wilhelmsens simply like this complicated structure, but the hoped for transactions, by and large, never occurred.

Today, just as in 2016, Wilh. Wilhelmsen Holding ASA shares trade at a >50% discount to asset value. But shareholders still realized a good return because the value of the underlying assets grew at a healthy rate. This is where I think most sum-of-the-parts/discount to asset value investment ideas go wrong: too much emphasis on the current discount to NAV, too little actual analysis of the underlying assets and whether they are likely to grow in value. Most companies that trade at big discounts to asset value deserve the discount. Either their assets are crummy and unlikely to perform well, or management is incompetent or dishonest and will destroy value or siphon it away. Wilh. Wilhelmsen ASA, on the other hands, owns good assets and manages them well, despite the internecine squabbling, and that is why investors have enjoyed good returns.

When you own deeply-discounted quality, you can be unconcerned with the pacing of a value-unlocking event. The assets are working for you. But when you own deeply-discounted garbage, every day that goes by before a value-locking event costs you the what you could have earned from owning a good asset. Better hope and pray that event comes along quickly!

One more item that caught my eye looking through my old stock pitch. I argued that Wilh. Wilhelmsen Holding ASA shares were worth in excess of book value because they had a track record of out-earning their cost of capital, with a 10-year average ROE of 14%. In the long run, an investor’s rate of return from owning a business will converge with that business’s return on equity multiplied by the earnings retention ratio, plus the average shareholder yield (dividend yield +/- net share issuance yield.) That is almost exactly what has happened with Wilh. Wilhelmsen Holding ASA shares, and it mattered far more than the discount to asset value that so fascinated me in 2016.

Looking Backward

Being a massive stock and business nerd, I enjoy reading up on the history of various companies I either own or find intriguing. Because I tend to invest in stodgier businesses and industries, many of them have been around for many decades and have some stories to tell. A few weeks back I snagged this corporate history published by one of my holdings, Monarch Cement.

The books consist mostly of media items on Monarch and its community. I could go on for hours about the fascinating news items, but here are a couple items of interest just from the first few pages.

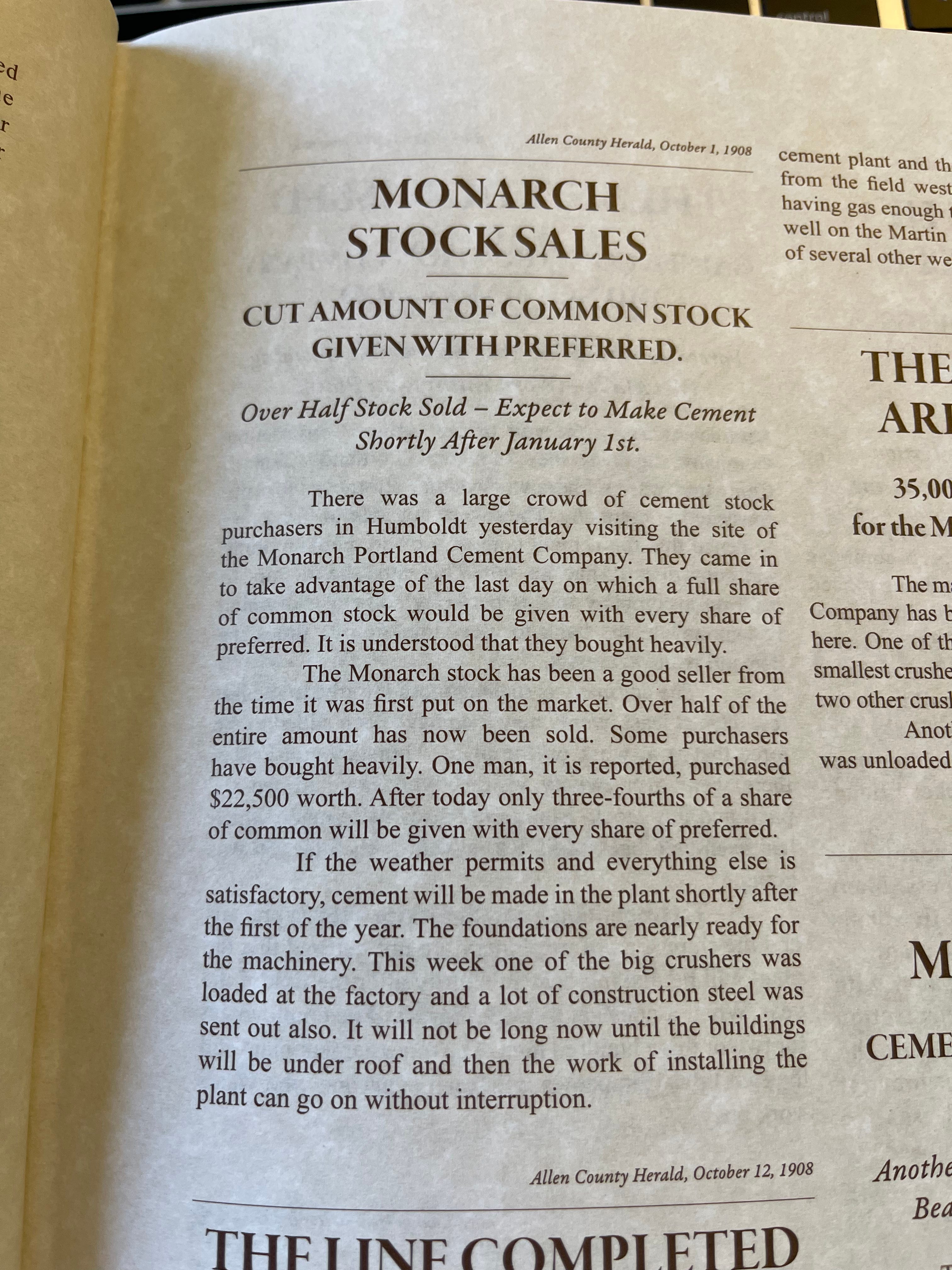

Raising capital in 1908 sure seems like more fun than it is today. I love the image of people physically lining up outside a company to buy shares. I also love the “ticking” feature where you get a full bonus share if you buy now, but only 3/4 tomorrow and presumably less not too long after that. Everybody hurry down! It’s probably for the best that public offerings are so much more heavily regulated today, but something of the magic has been lost. I wish there remained some mechanism by which a company could easily offer securities to community members.

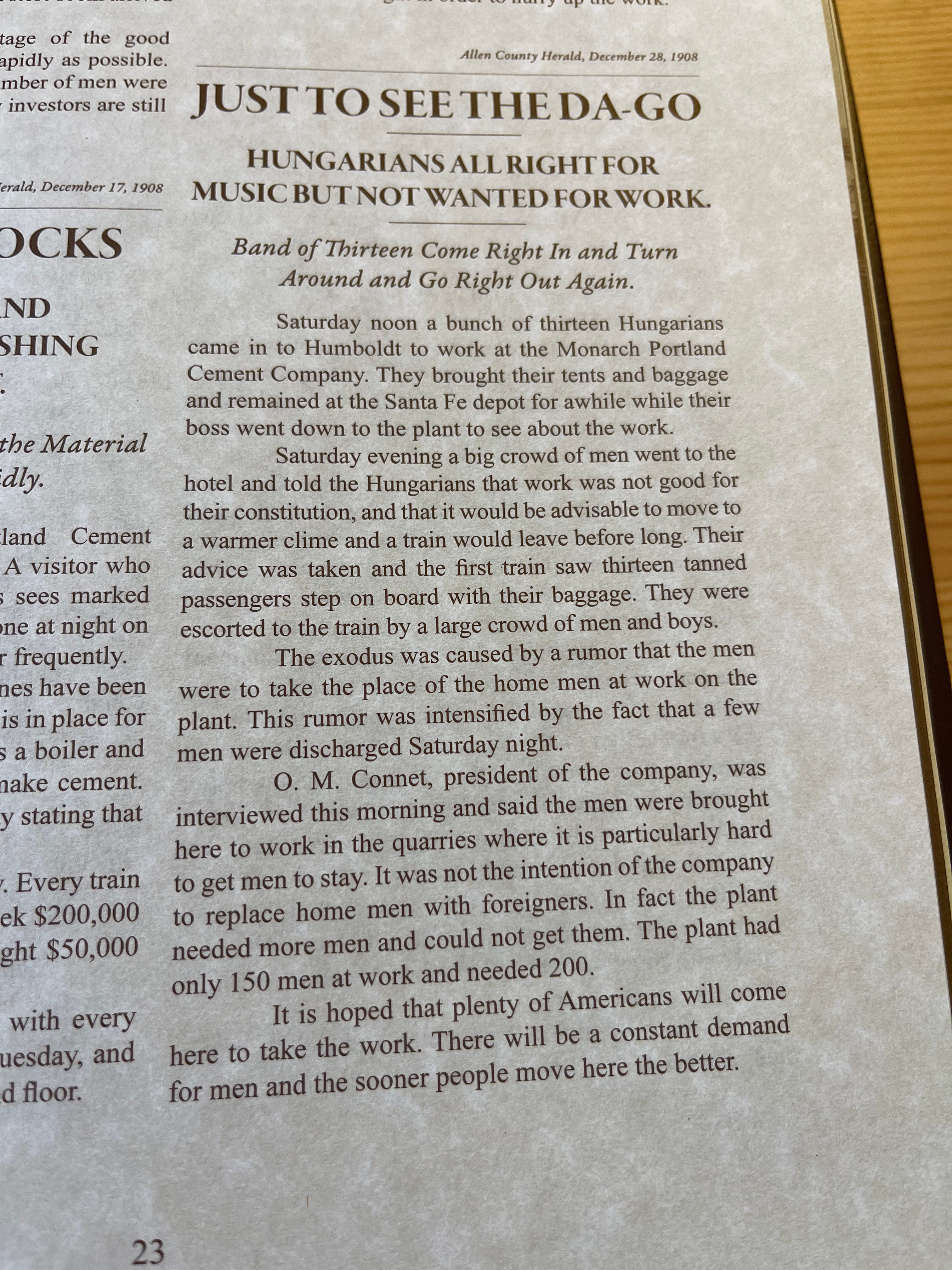

Credit to the company for not shying away from the troubling parts of local history. Here they include a news item that describes local men running off members of an ethnic minority who were looking for work at the plant. The Allen County Herald headline even includes what appears to be a pun on an ethnic slur, though the slur is being applied more broadly than is typical. Perhaps the reporter was not overly concerned with the details of the ancestry of the job-seeking men? While shocking to those of us reading today, its worth remembering just how prevalent these prejudices were in the early 20th century. I can remember my own grandfather describing the ethnic hierarchy of his Pennsylvania coal town in the 1930s. Though they were all as poor as the dirt they dug, those of Western European descent held themselves above those of Eastern and Southern European ancestry. (People of other racial and ethnic backgrounds were rarely encountered, let alone esteemed.) While racism and prejudice are alive and well today, good riddance to this particular corrupting strain.

Et Cetera

It’s been a little while since I wrote here, so I thought I would post my Q2 letter. In addition, Alluvial has some cool stuff in the works that I hope to be able to discuss soon. I am always looking for more investment ideas and/or just plain weird investment stuff to discuss, so please don’t hesitate to e-mail me or message me on Twitter. I make every effort to respond to all the e-mails I get, but I get a lot so sorry in advance if your message slips through the cracks. Just give me a nudge. Thanks for reading!

Alluvial Capital Management, LLC holds shares of Four Corners, Inc. and Monarch Cement Co. for client accounts it manages. Alluvial Capital Management, LLC may hold any securities mentioned on this blog and may buy or sell these securities at any time. For a full accounting of Alluvial’s and Alluvial personnel’s holdings in any securities mentioned, contact Alluvial Capital Management, LLC at info@alluvialcapital.com.

Dave does not mention the biggest flag about Four Corners: It is incorporated in Nevada.

Hi Dave, a new reader to your substack. Enjoyed the writeup. To follow up, I have a doubt which I hope that you can clarify/shed light upon and I hope I am not asking much of your valuable time. Imagine a company that is competitively strong vs peers, growing and in a go-go industry that is expected to continue enjoying the tailwinds infinitely to the future. Despite such an description, if management or controlling shareholders of the company engages in questionable activities, or displays lack of ethics (for eg-scooping off revenues/value generated in form of costs/rents to related parties, family members; employing incompetent people across the board/management to oversee business; cheap capital access/siphoning to controlling shareholders/management in form of cheap loans etc.), what would be your approach to valuing/investing in such a company? Would you price in the possible risks in your valuation estimate, or completely steer clear from such companies even if they are available for huge discounts?