Ocean Yield ASA - OCY:Oslo / OYIEF:OTC

Just a quick post today to talk about what I think is a very interesting company - Ocean Yield ASA. The company was created in 2012 from assets owned by the Norwegian industrial giant Aker ASA, which remains the majority shareholder. Ocean Yield's business model is very simple: it purchases ships, then leases them to high-quality global shipping companies under long-term charters. In order to deploy more earning assets and produce a more attractive return on equity, Ocean Yield employs meaningful leverage. Ocean Yield pays out the majority of its earnings in dividends (hence the business name) and strives to increase the dividend as its fleet grows.

This is the business model employed by nearly all leasing companies, as well as banks. Borrow short, lend long, and earn the spread. There are risks to this business model, but first let's take a look at the types of ships that Ocean Yield currently owns. The company's fleet is modern and fuel-efficient, crucial to ensure the vessels will have strong residual values once their leases are concluded.

Chemical tankers make up roughly one third of the fleet. Chemical tankers are specialized ships that tend to see more stability in dayrates, making them an attractive sector for Ocean Yield. Since its founding, Ocean Yield has growth its fleet at a steady pace. The company intends to grow its fleet by $350 million annually. Fleet expansion is funded operating cash flow as well as debt issuance.

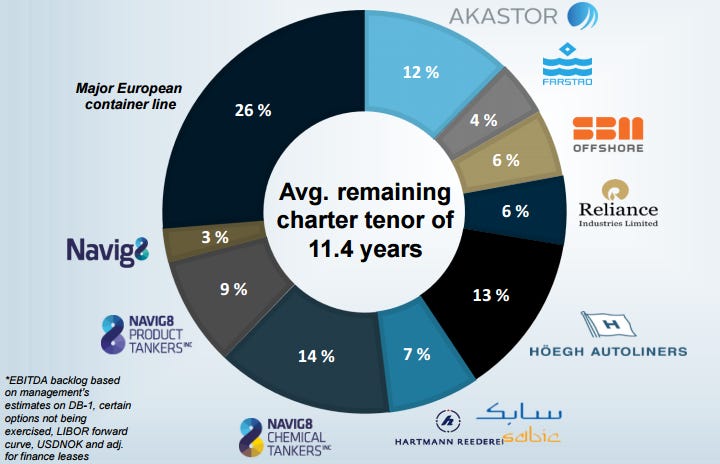

Just like a bank making loans, Ocean Yield seeks to lease its ships to highly creditworthy shippers. Below is the breakdown of Ocean Yield's counterparties. The list is rather concentrated, but these shippers do represent some of the largest and best-capitalized around. Ocean Yield's average charter term is quite long at 11.4 years at quarter's end. Some of the leases include purchase options or other customizations that make the lease more attractive for the ship's operator.

The credit performance of Ocean Yield's lessees has been generally good. But being that shipping is a highly cyclical industry and shippers tend to carry high leverage, Ocean Yield has had to restructure leases on more than one occasion. Restructuring tends to involve accepting lower lease payments, and may result in receiving one-time cash payments or securities from the distressed shipper. Thus far, Ocean Yield has managed these disruptions without serious losses.

Counter-party risk is one major risk that Ocean Yield faces. Another is residual value risk. The annual earnings of each of Ocean Yield's ships is essentially its lease revenue less depreciation. But what happens if at the end of the lease, the ship turns out to be worth far less than its book value? That means that economic deprecation was higher than accounting depreciation, and accounting earnings exceeded economic earnings. That's a bad scenario. Ocean Yield must be careful to invest in ships that will maintain their value at least as well as their accounting depreciation schedule would success, in order to be sure that reported profits are not illusory. Ocean Yield must also take care to invest in ships that are not in danger of obsolescence due to changes in technology or regulations. A large write-down in a ship's value could wipe out a huge amount of reported profit.

The third major risk to Ocean Yield's business model is financing risk. Ocean Yield carries about $1.36 billion in net debt versus $2.32 billion in tangible assets. The company's equity ratio is 35.2%. Liquidity is good, as the company has $264 million of available liquidity. Still, the company would be negatively affected by rising interest rates or a disruption in credit markets.

Ocean Yield has a solid history of increasing revenues and profits since its inception. The fourth quarter of 2016 was a notable exception with a writedown on a vessel extinguishing nearly all profits. EBITDA declined from Q4 2016 to Q1 2017 because for one of the company's ships, Lewek Connector, the associated lease went into default and the vessel was re-leased at a lower rate while restructuring talks take place.

Nonetheless, profits excluding one-time items have continued to rise. The company has increased its dividend apace, and now pays $0.74 annually. Quarterly dividends have grown at an annualized pace of 14% since the first quarter of 2014.

On an annualized basis, Ocean Yield is currently producing earnings of 89 cents per share. Shares are quoted in Norwegian Krone, but the company operates in US dollars. The current share price of NOK 65 is equivalent to USD 7.70, for a P/E ratio of 8.7 and a dividend yield of 9.6%. Both Ocean Yield's earnings and dividend could rise as the year progresses once the company's newbuild containerships and gas carrier begin contributing. In addition to the already announced fleet additions, the company maintains its $350 million fleet growth target.

So, what's it worth? I never like to pay too much for leasing companies. They don't typically enjoy significant operating leverage as they grow, and like other leveraged business models, there is always the risk of a blowup if they get too aggressive on the lending/leasing side or if credit markets lock up. Ocean Yield does have the benefit of a deep-pocketed backer in Aker ASA, but the risk is never entirely mitigated. A lot depends on the company's efforts to grow its fleet responsibly and avoid over-paying for ships. Still, I do think the company's good track record deserves a valuation higher than 8.7x trailing annualized earnings. I would be happy to buy shares up to 10x trailing earnings, which works out to 1.6x book value. Some might ask why a business made up of nothing but ships which anyone can buy should be worth more than book value, but I would counter that expertise in leasing and navigating the complex world of global shipping is worth quite a premium. Ocean Yield and other lessors seem to be providing a valuable service where traditional banks have withdrawn. At least for now, Ocean Yield is capable of earning a high return on equity, and that merits a premium to book value.

Alluvial Capital Management, LLC does not hold shares of Ocean Yield ASA. Alluvial may buy or sell shares of Ocean Yield ASA at any time.

Alluvial Capital Management, LLC may buy or sell securities mentioned on this blog for client accounts or for the accounts of principals. For a full accounting of Alluvial’s and Alluvial personnel’s holdings in any securities mentioned, contact Alluvial Capital Management, LLC at info@alluvialcapital.com.